")

The Buy Now Pay Later (BNPL) was once the fastest-growing part of the financial services industry. It is home to the UKs, fastest-ever unicorn, Zilch, which went from zero to a billion-dollar valuation in 14 months!

The industry rode several waves, for instance, the e-comm boom during COVID, access to cheap capital and bullish valuations from institutional investors.

In addition, it remains an unregulated product (in the UK), unlike its cousin, the payday lenders had heavy regulation imposed.

It all but thrashed major players like Wonga and Amigo. At the same time, it was giving BNPL players ‘white space’ to grow.

And boy, did they grow. During their heyday, lending via BNPL went from $2 billion in 2019 to $24 billion in 2021.

However, today the industry is unrecognisable.

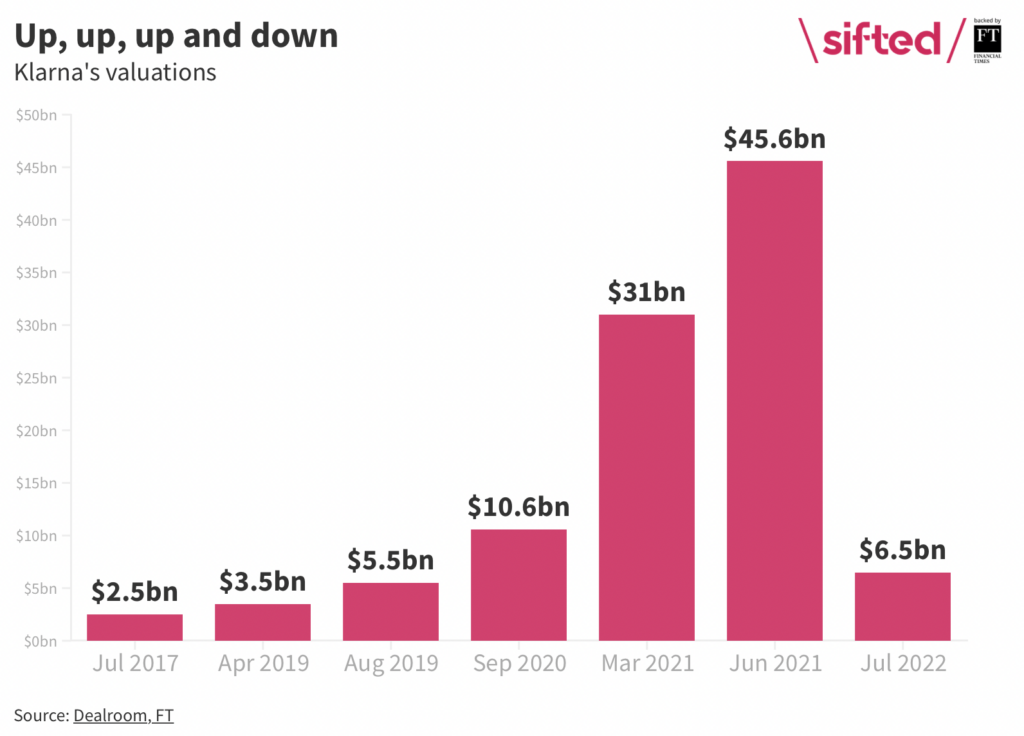

For example, Klarna’s valuation has slid from c$60 billion to a mere $7 billion.

Moreover, shares in another firm, Affirm from the States, are down 80%. Even Zilch has been unable to stand the changing tide, with significant layoffs being reported.

The root cause?

Multiple factors are all around us. From an end of cheap finance to spooked investors halting lofty valuations. All of which is dramatically increasing the cost of capital.

On the other hand, a cost of living crisis bites large consumer purchases, and a recession makes the payback of the loans less assured.

The final headwind is the constant regulatory scrutiny that leaves the industry vulnerable to going the same way as its cousin, payday loans.

It’s the perfect storm for this industry, and the significant players are caught in its eye.

So the question is, does it have a future?

You wouldn’t think so, right? Well, I think, think again. Let me explain.

First, there is one significant difference between BNPL and payday loans.

And that most don’t charge interest to the consumer on purchases.

Even the late fees recently introduced by Klarna are arguably reasonable compared to the payday loan equivalents.

Secondly, consumers of all demographics are buying this product with great frequency.

The Centre for Financial Capability study shows that all demographics used the product.

But more encouraging is that younger people primarily use it.

With this level of demand, it will likely continue, perhaps not in the current guise we will come onto.

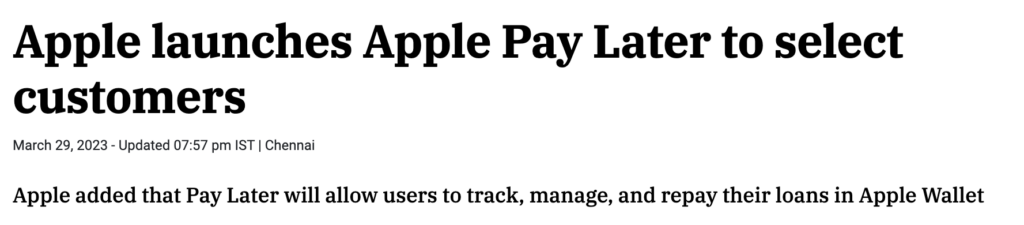

Thirdly, despite the issues, several players have entered the space. For instance, Apple Pay Later is being trialled to select customers throughout the US. Whilst significant payment providers like Mastercard have also gotten into this space.

Undoubtedly, the industry needs to consolidate to survive and it will. It will look like a very different industry on the other side, with some serious winners and losers.

Here is what I think will be required in the next iteration of the industry:

1. Regulation

The regulator will play a more significant role across the industry. For instance, in the UK, the Financial Conduct Authority has already been active in regulating BNPL players’ communications.

They are particularly interested in misleading wording that leads to vulnerable groups using these services.

In a similar vein as Payday loan regulations, they will be to protect the consumer interest, including keeping interest rates fair.

2. Risk management

There will be greater scrutiny of the customers that these services will be available for. We have already seen the beginnings of this with Apple’s Pay Later service, and there is no doubt it will continue.

Interestingly, another fintech, Kriya, a specialist in Invoice Finance, recently undertook an end-to-end audit of their debut book. This is mainly in light of the recent issues related to Silicon Valley Bank.

I can imagine the BNLP players doing a similar audit and restricting services to customers who do not pay on time.

3. First-party data

In the next iteration of the industry, only those who can leverage first-party credit scoring data will likely remain hyperactive. Data will indeed trump everything else in this space.

Summary

It’s certainly a tough spot the industry finds itself in, and it’s not looking bright any time soon. But those that can weather the storm will indeed benefit from the fruits of their endurance.