The basic aim of marketing segmentation is to try and reach the customer in the most impactful way at the right time, and in the right place.

Marketing has evolved from being just a product and service description mechanism to becoming a platform through which businesses engage their audiences, connect with them, and attempt to resonate with their thinking. The ability of businesses to communicate with customers and understand their buying patterns, points of view, likes and dislikes, and preferences through evolving marketing capabilities, is something businesses should look to leverage.

The aim of developing a customer-centric marketing strategy is to build and nurture long-term relationships with both existing and new customers, and this is achieved by putting the customer at the heart of every business decision you take. It involves:

Businesses that take decisions keeping the customer at the core of their thinking, often experience higher customer lifetime value (CLV) and lower customer churn, both proving to be tremendously lucrative in the long run.

Becoming a customer-centric organisation, however, is a slow process and businesses have to continually take small steps to strive in that direction. They have to approach becoming customer-centric as something that is a constant ‘work-in-progress’, and they cannot afford to be complacent in this regard. Strategic marketing gives a business the opportunity to provide consistently positive customer experiences. However, to achieve this with optimum resource utilisation requires strategic thinking and planning.

Strategically planned and executed marketing efforts give a business the platform to understand their customers, which is the first step in becoming customer-centric, provided that the business has decided to make that a priority. The interactive nature of marketing today has given businesses an unprecedented ability to delve into their customers’ requirements, preferences, struggles, motivations, and it provides businesses a way to understand how they can add value to the customer’s life and, in turn, increase the CLV for the business.

What is segmentation:

The principle of standardisation vs personalisation:

You have likely heard of products that are ‘one-size-fits-all’. Perhaps there is no better example than Henry Ford’s famous quote referring to the revolutionary T-Model Ford automobile in the United States, in the early 1940s, as, “You can have any colour [car], as long as it is black”.

In essence, the approach was to develop a standardised product that could be sold across the world, where both the customer and company could benefit from the economies of scale achieved. It enabled Ford to offer a consistently high-quality product at a cost-effective price in a short production time.

However, this approach is unlikely to work in the present-day context. Most automobile manufacturers aim to appeal to a global market, whilst catering to the specific needs of customers across segments. This ‘glocalisation’ approach requires manufacturers to tailor their product to meet the needs and preferences of the local market. It’s important, for instance, to consider which side of the road customers drive on, the national safety requirements of the country, and the features that customers from a particular country, or region, might prefer to have their cars fitted with.

Therefore, in order to remain competitive, global manufacturers need to ensure that they meet the specific needs of customers at a local level through personalisation. The outcome of personalisation and localisation is that companies are unable to achieve the same level of cost-efficiencies, and therefore it is more expensive to implement. This has a knock-on effect on the following:

1. The cost to produce the product for the company

2. The cost to purchase the product for the customer

Therefore, the optimal product strategy looks to gain a balance between cost-efficiencies and personalisation, in order to meet customer need. The good news is that in today’s digital context, it is possible to achieve personalisation on a mass scale, known as ‘mass customisation’.

If we return to the example of the automobile industry, mass customisation has become so commonplace in developed markets that personalisation has arguably become a basic customer expectation, rather than a key brand differentiator. Increasingly, even vehicles targeted at low-income groups have a range of customisations that would have been deemed as ‘luxury add-ons’ for much more expensive vehicles in years past, because of advances in efficiency and reduced costs. Digital technology enables this trend as organisations allow customers to customise their preferences like never before, so much so that people are willing to buy a car without even having stepped foot inside it!

The question becomes, ‘how do companies understand and deliver what customers are looking for?’ This is where segmentation strategies become critical.

Definition of Segmentation

Developing and delivering products and services that meet customer need in the most efficient way is at the heart of customer segmentation. Consider the consequences if we treated every single customer as an individual and manufactured a product just for them. Although, this would probably lead to a high degree of customer satisfaction, a company is likely to be unable to deliver this in a cost-effective manner, and the product would not be viable over the long-term.

Segmentation looks to bridge this gap, enabling companies to group customers with similar needs and wants together. Understanding the unique set of needs and wants of different customer groups is key to developing a product that best satisfies the end consumer.

Finally, one needs to remember that these segments are not static, as customers’ circumstances and needs change over time. Operating a segmented approach in this way allows customers to easily move from one segment to another, as circumstances and needs change.

Why segment customers?

Segmentation is the cornerstone of a successful customer-centric strategy, as it recognises that customers’ needs and wants differ from each other. Crucially, if we are going to be successful, then we must understand and meet those needs and wants, as they change and evolve over time. Let’s explore this notion in greater depth:

- Customer preferences

Preferences help determine the type of product and service to offer. To highlight this, let’s take the example of a typical student current account offered by a bank. The features and benefits are all aligned to what a student would require and find appealing. For instance, they may get an interest-free overdraft, or a student railcard to travel from university to home. Service levels, however, might be different from that of a premium customer, who might have access to a relationship manager, whilst a student might be able only to bank online, or on their mobile. By delivering customer preference, customers will feel valued and delighted by the product or service. This will, in turn, lead to increased customer loyalty and advocacy.

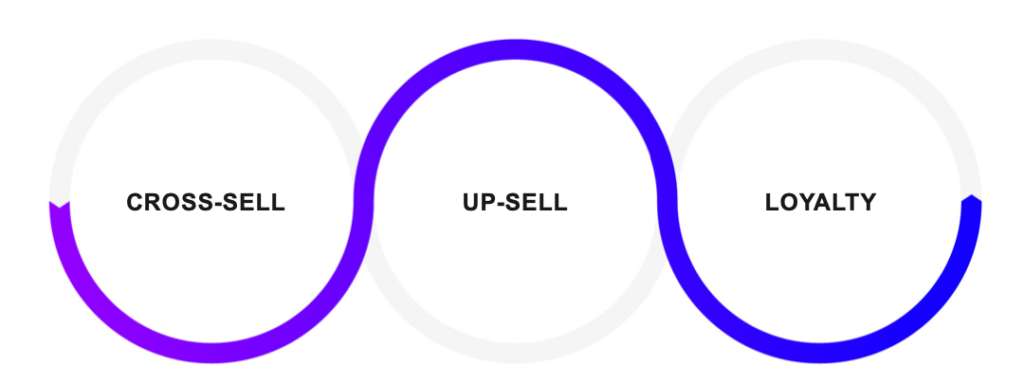

2. Customer value

At the heart of every business is the desire to increase overall customer value by increasing the breadth and depth of the relationship that the customer has with the business, over time. If we can design products and services that delight our customers, we will be able to execute the following three key strategies that help in our pursuit of increasing CLV:

Cross-sell

We will be able to sell more than one product to a customer through effective cross-selling. This is often measured in terms of product penetration, per customer. Traditionally, customers would be acquired through a current account and then cross-sold a range of other products such as savings accounts, lending, and investment products. The logic being simple: The more a customer buys from you, the more profitable (and hence valuable) the relationship.

Up-sell

In many industries, but particularly in financial services, customer needs are ever-evolving and hence the need to conduct frequent financial reviews. This not only ensures the product constantly meets customer need, but presents the opportunity to up-sell an existing product with one of higher value, if the customer’s circumstances have changed. Offering a customer a higher level of service will increase their overall satisfaction, and make them more loyal to the organisation.

Interestingly, a higher value package may not always be more expensive for the customer. Take the example of a mobile phone contract. It usually comes with a limited number of inclusive minutes, texts, and data. However, if usage falls outside limits, there will be additional charges. Seeing this and simply putting a customer on a more appropriate tariff could actually save them money and greatly increase satisfaction. It works the same way with financial services, and will help foster the relationship over the long term.

Loyalty

In order to exist and succeed, a financial services company requires customers to stay with them in the long term. The easiest way to achieve this is by ensuring you meet customer need better than the competition. This will lead to recurring revenue for the organisation and the company will not have to constantly rely on finding new customers that are often more expensive to acquire and service than existing ones.

Customer loyalty is therefore essential for financial services companies, and they achieve this by aligning their products and services to meet the customer need.

Interestingly, achieving loyalty doesn’t always mean having to offer the cheaper product or service. Many customers will base their purchase and retention decision on a range of factors, including brand, service, experience and benefits, and not just price.

Therefore, to build customer loyalty, one must look at the relationship across all customer interactions and ensure that you are meeting customer need on all levels. Whilst this is often difficult to achieve across the business, consistency is key. If a customer receives a consistently high level of service in all their interactions with your brand, then they will develop a much more favourable brand perception, and are more likely to remain loyal.

3. Commercial imperative

We have already mentioned the need for organisations to ensure that they make a profit. Segmentation allows organisations to vary the product and service levels in such a way that they are able to achieve this objective, whilst still meeting customer need.

Joe Garner often used the analogy of running an airline. For an airline like British Airways to run smoothly, efficiently, and profitably it needs passengers from First Class to Economy. It’s unlikely that the airline would be able to operate a viable commercial proposition without either segment. Along the same line, companies from banks to FMCG companies have to assess the customer portfolio and make-up of their customer base keeping the commercial imperative in mind.

4. Product strategy

Fundamental to the successful strategy of a financial service institution is the need to carefully craft its value proposition and product portfolio to align with different customer segments.

At the heart of this approach is determining how best to leverage the internal business capabilities and existing synergies across all products within the portfolio, whilst personalising certain aspects of the products that appeal to different customer groups.

However, if we were to look beneath the bonnet, quite literally, we might see a range of commonalities between both vehicles. The chassis and engine are identical, whilst the look, feel, features, and benefits are very different. Therefore, they have been able to achieve both cost-efficiency and personalisation through this approach.

Different Ways to Segment Customers

We have explored segmentation and the reasons it’s important for an organisation to use this approach. Let’s now turn to how organisations can go about segmenting their customers.

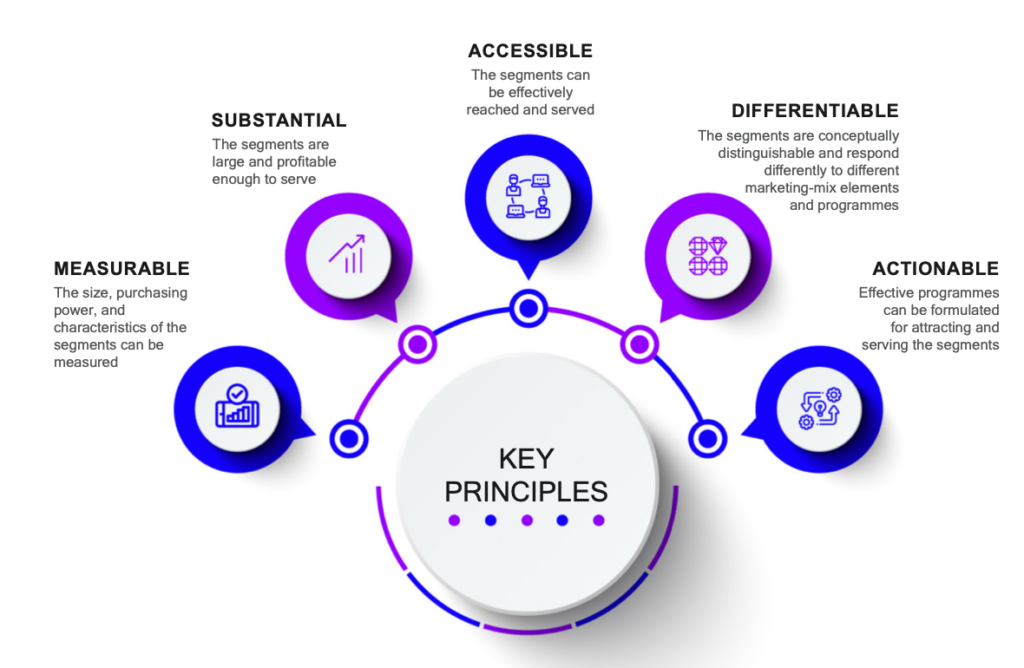

In reality, there are countless ways that organisations can choose to segment customers. We will focus on the dominant methods. Before we begin, it’s important that we understand the five key principles that make up an effective segment, according to Kotler (2003):

We will explore four different segmentation strategies in this section.

- Geographic and Demographic Segmentation

Traditionally, segmentation strategies have focussed on grouping customers based on a range of attributes and characteristics that were identifiable. In the case of geographic segmentation, groups are divided based on different geographical units such as regions or clusters.

On the other hand, demographic segmentation is used to divide customers based on variables such as age, family size, family life cycle, gender, income, occupation, education, religion, race, generation, nationality, and social class. Often, data you can derive from the national census forms part of demographic segmentation.

2. Psycho-graphic Segmentation

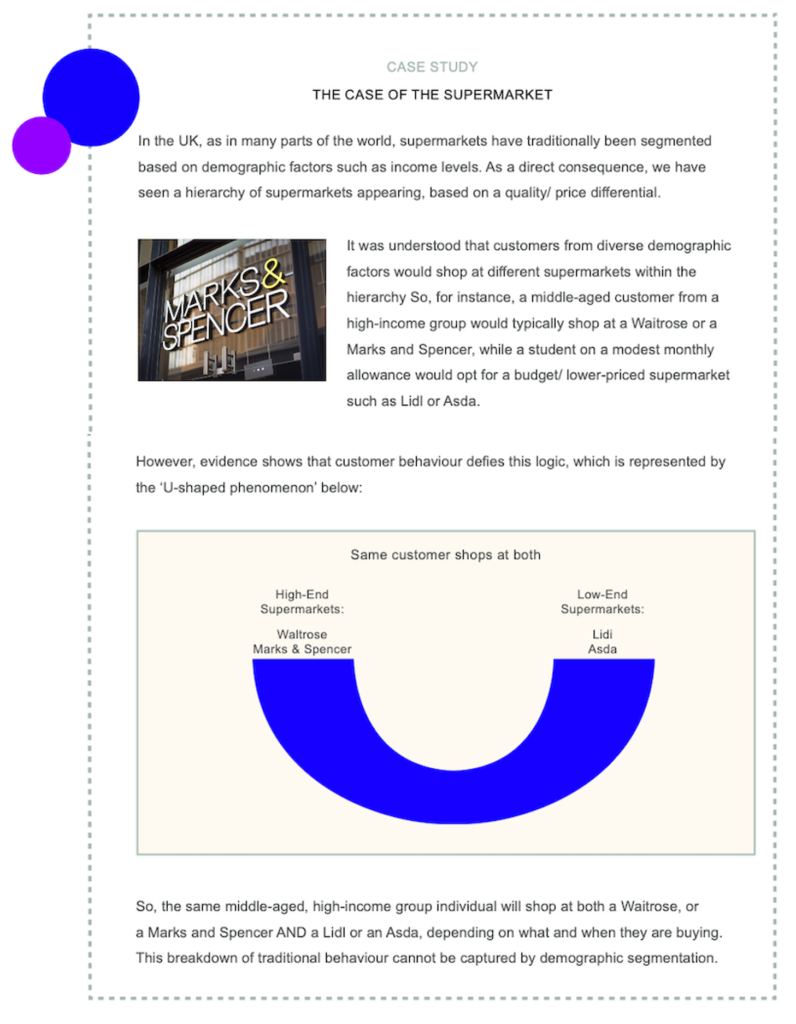

As we have noted in the mini case study on supermarkets, the way customers shop has changed dramatically, and it was difficult to capture the trend by simply using traditional demographic segmentation. This is because the shift occurred at a more fundamental level that cut across demographics.

Ultimately, the shift in shopping behaviour can be attributed to a combination of changing attitudes, lifestyles, personalities, and values of customers. It is therefore important that we use each of these attributes to classify customers and create segments.

3. Lifestyle

According to Kotler (2003), lifestyles are partly shaped by whether consumers are time constrained or money constrained. These dimensions will influence a certain key set of actions and beliefs, relating to lifestyle. There are a range of other factors to consider, for example, whether someone is culture-oriented, sports-oriented, or outdoor oriented (Kotler, 2003).

4. Personality

Marketers often reflect a consumer’s personality in their brands. This helps create a sense of kinship between the target consumer and the brand. According to Kotler (2003), a brand may wish to appear sincere (Gateway Computer), exciting (Nike), competent (Hewlett-Parkard), sophisticated (Lexus), or rugged (Timberland).

In addition, as is often the case within the Financial Services, or in the FMCG context, companies operate a brand portfolio strategy to attract consumers from more than one segment. They use brand personality to differentiate each of them.

5. Values

According to Kotler (2003), some marketers segment by core values: the belief systems that underpin consumer attitudes and behaviours. Core values go much deeper than behaviour or attitude, and determine, at a basic level, people’s choices and desires over the long term. Marketers who segment by values believe that by appealing to people’s inner selves, it is possible to influence their outer selves: their purchasing behaviour.

6. Customer value

One of the most important pieces of information an organisation needs to know about their customers is their level of profitability: both current and potential. This helps them make key strategic decisions relating to the products and services they offer them.

Often, organisations will cluster customers into tiers such as high, mid, and low-value, as well as making certain allowances for potential, or future value. This enables the company to make judgements about the level of investment they will make per segment and, broadly, how they will move those segments up the chain.

One organisation classified all their customers into high, mid, and low-value segments and then created a three-tier strategy for each segment. The strategic aim for the high-value segment was to protect those customers from leaving. This could mean offering them higher levels of service and/ or additional proposition features and benefits. It was the highest priority to delight these customers in any way possible, as they generated the highest amount of profit for the bank.

The strategic aim for the mid-segment was to grow the value of these customers. It was likely that these customers had other products with competitors and the bank aimed to increase the amount of product penetration, per customer. For example, this may have led to special offers or promotions on select products for this segment, in order to win more business from them.

Finally, the strategic aim of the low segment was to determine the potential for them to move into a higher tier segment in the future (e.g. students), or divest the relationship, if it was deemed unprofitable.

7. Behavioural

One of the biggest issues marketers face when conducting customer research is when a customer says they will act a certain way and then, when it comes down to it, they act completely different. It’s therefore important to base decisions on certainties—what is actually happening, rather than what someone has said might happen. This is where behavioural segmentation comes to the forefront.

It looks to cluster customers into similar groups based on similar actions or behaviours (rather than basing it on any characteristic or indicator). For instance, the channel of choice, or usage, in an insurance context is a powerful indicator for both pricing and attrition levels.

Many companies will segment customers by channel of entry. For example, those who purchased products over the phone will be segmented into one group, whereas those who made purchases over the internet will be segmented into another. The fact that customers exhibited a similar behaviour determines the segment, rather than any other characteristic.